Roof Repair Depreciation Life

What Is The Depreciation Of The Roof On A Commercial Building

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Part Three The Value Of Accurate Roof Age In Claims

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

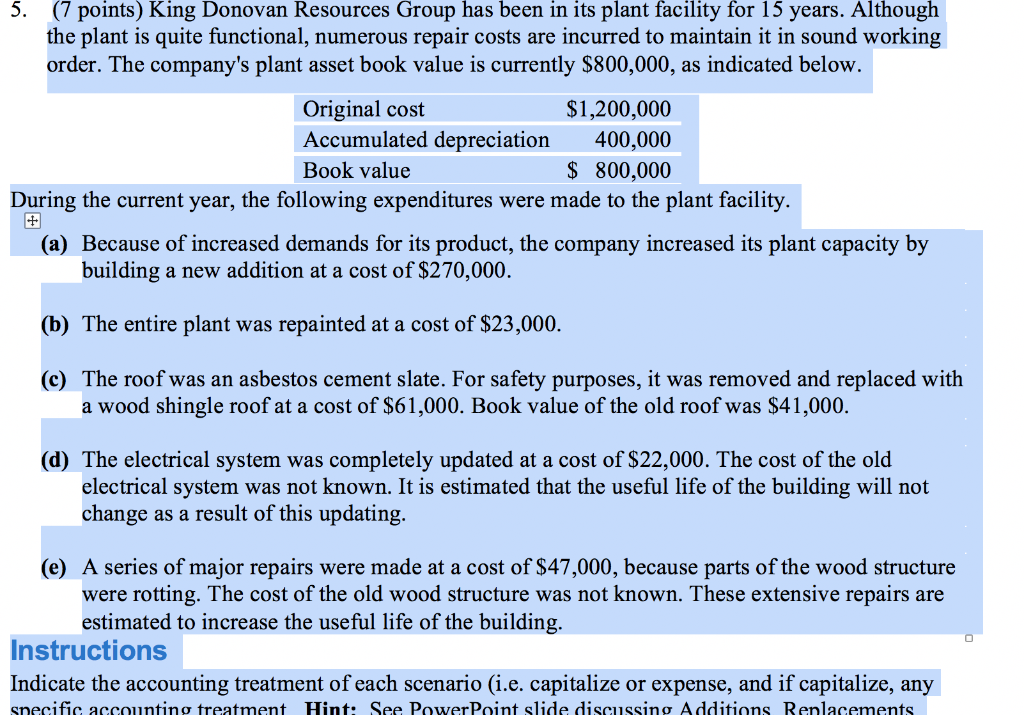

Solved 7 Points King Donovan Resources Group Has Been I Chegg Com

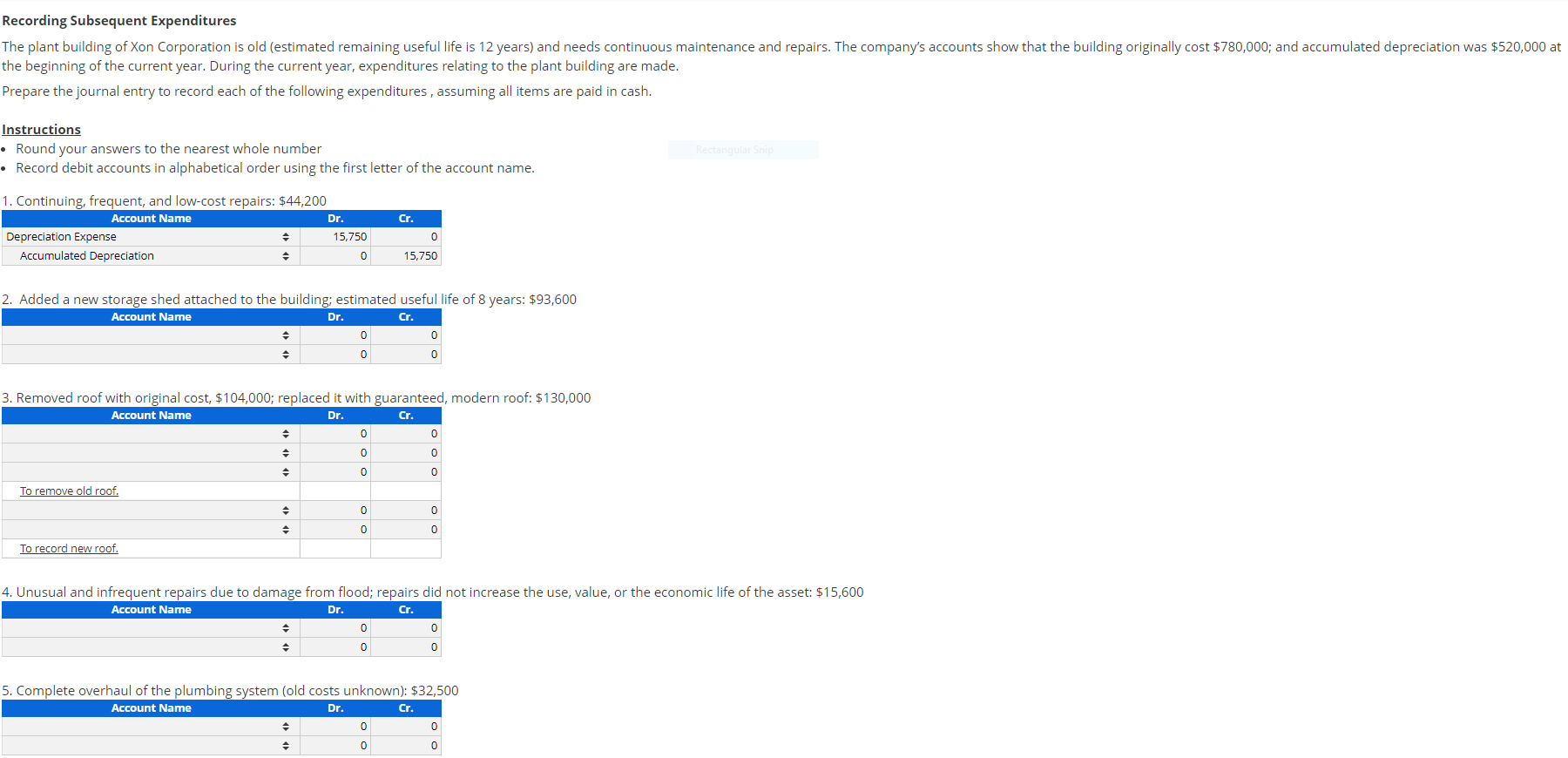

Recording Subsequent Expenditures The Plant Buildi Chegg Com

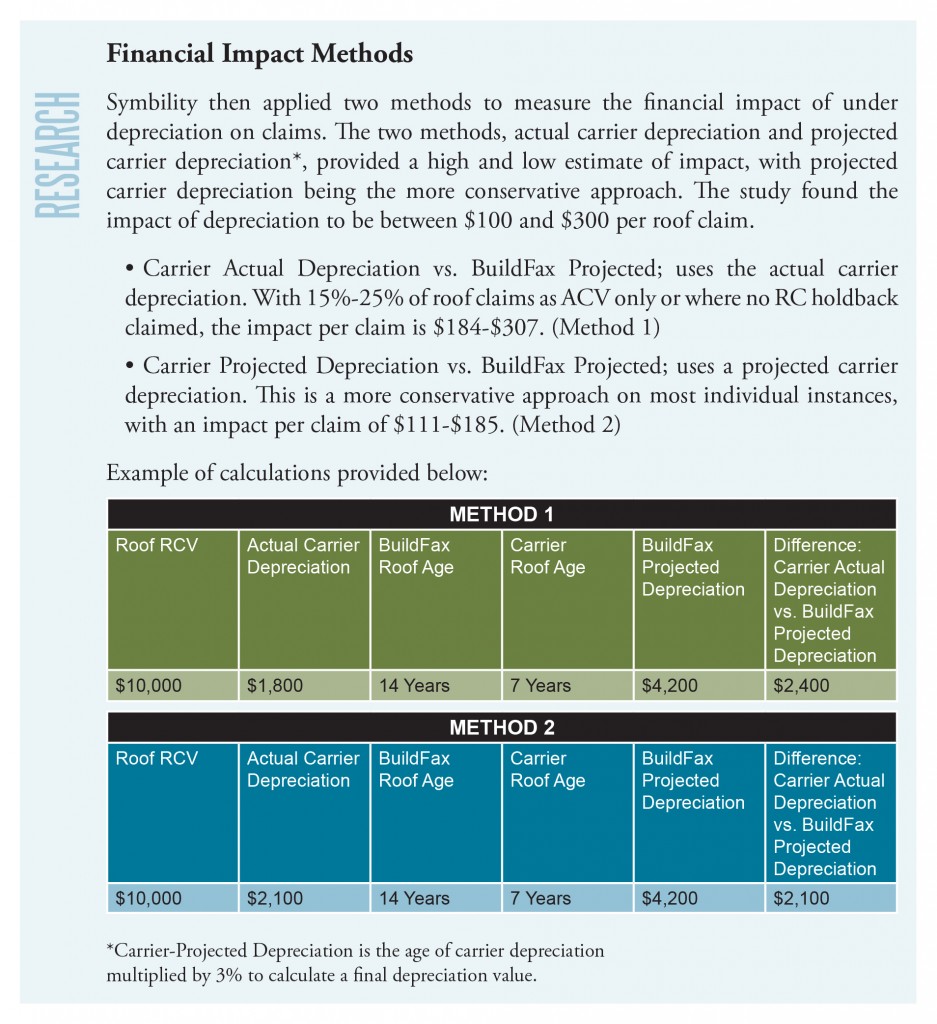

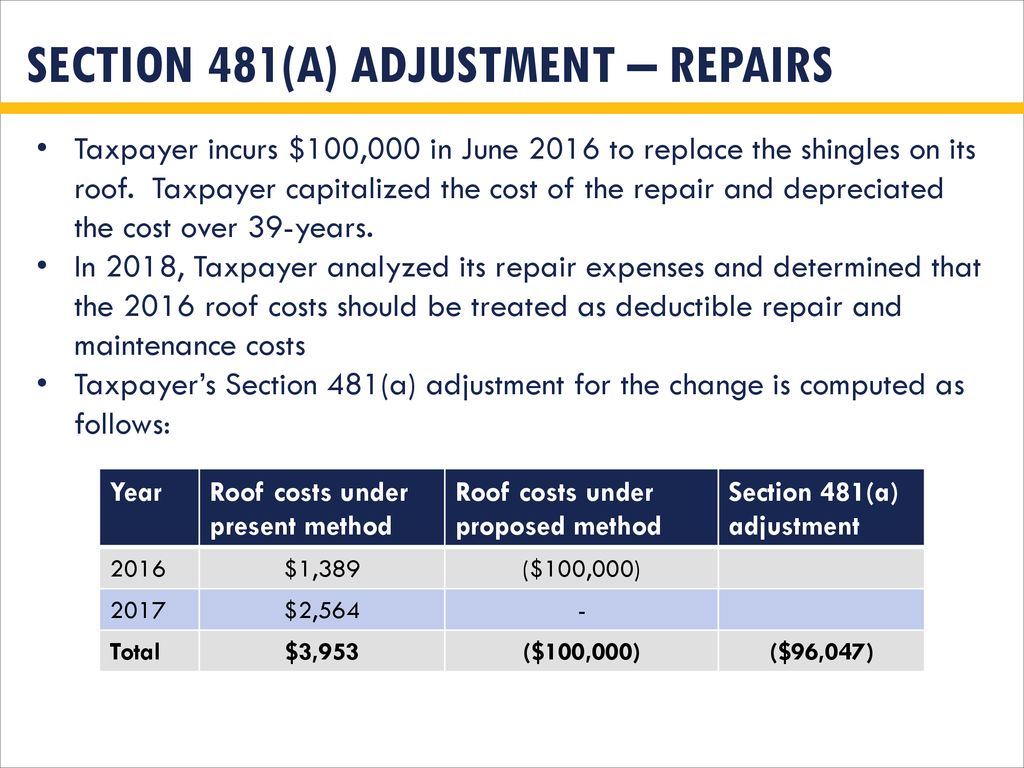

The full replacement cost of the roof is 10 000.

Roof repair depreciation life.

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin Insurance Deductible Home Insurance Insurance Marketing

Rcv Vs Acv Whats The Difference A Young Insurance Agency Inc

Https Www Calt Iastate Edu System Files Premium Video Files Rr 20dispositions 20 203 20per 20page Pdf

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

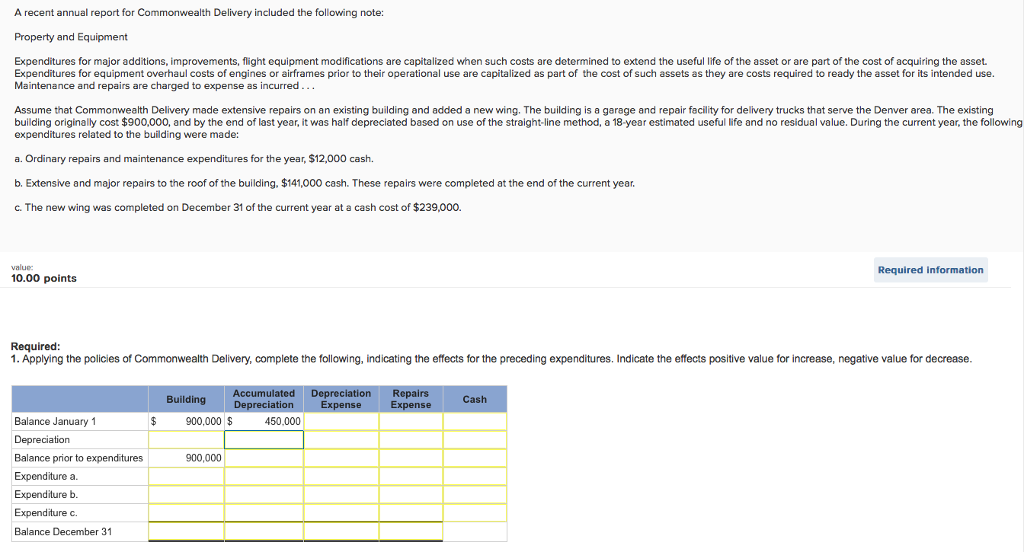

Solved A Recent Annual Report For Commonwealth Delivery I Chegg Com

Rental Property Depreciation Rules Schedule Recapture

How The New Tax Law Affects Rental Real Estate Owners

Depreciating Labor Costs The Rough Notes Company Inc

Homeowners Insurance 101 Roof Age Matters At Claim Time

179 Tax Deduction For Commercial Roofing Projects Advanced Roofing Inc

Can I Make Money Off My Insurance Roofing Claim Slade Roofing

Recapitalization Capital Renewal What S The Number Tradeline Inc

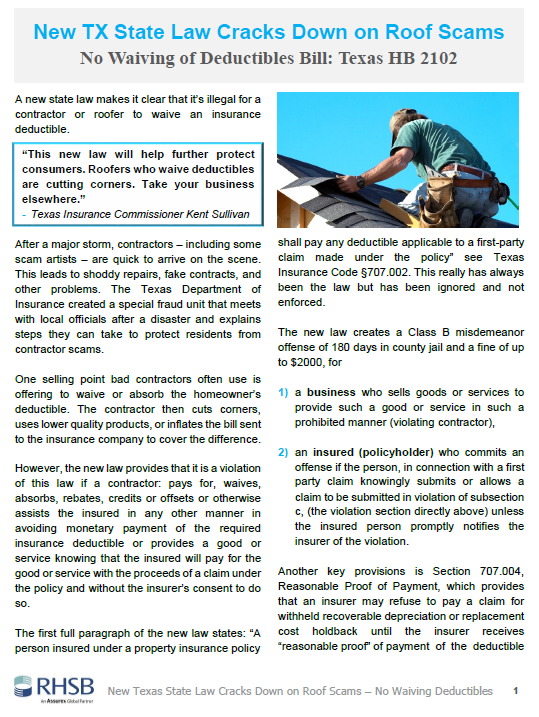

New Tx State Law Cracks Down On Roof Scams No Waiving Deductibles Rhsb

Accounting Method Changes Post Tax Reform Ppt Download

Pin Di Destinasi

Roof Insurance Acv Vs Replacement Cost Bankrate

How To Get Insurance To Pay For Roof Replacement Rgb Construction

Guide To Expensing Roofing Costs Expense Vs Capitalized Bergankdv

Overview Of The Cost Approach Final Reconciliation Ppt Download

Section 179d Tax Deduction For Commercial Roof Replacements

Hospitality Capex Math 101 Useful Life Cayuga Hospitality Consultants

Roof Insurance Claim Denied

How Long Does A Roof Last Age Of Roof And Insurance Harry Levine

What Residential Roof Warranties Will Cover In Kansas City Pyramid Roofing

Source : pinterest.com